The most recent MPE Berlin was, as ever, an intense and productive affair. Over three days in March, more than 1,600 participants, including over 400 merchants, gathered in Germany’s capital from 52 countries across the globe.

This year’s conference bore witness to the growing dynamism of payments as an industry. Not only were more than 7,000 one-to-one meetings booked through MPE’s dedicated app: there were also more than 15,000 private chat messages exchanged and almost 4,000 QR-code scans as people met informally in coffee areas, break-out rooms and corridors, exchanging details and building their networks.

“Over three days, more than 7,000 1-1 meetings were booked through MPE’s dedicated app.”

We spoke to some of the leading voices in European payments who came to MPE 2026, asking them for their thoughts on this year’s conference, the challenges merchants face today – and what to look out for over the next 18 months in payments.

“MPE’s programme reflects what’s actually happening in the industry now – as well as focusing on the future.” – Miranda McLean, Chief Marketing Officer, Ecommpay

Leaders we spoke to for this article acknowledge MPE as unique among payments conferences, since it brings together merchants with payments providers and banks – effectively, the entire payments ecosystem under one roof for three intense days. As Miranda McLean, Chief Marketing Officer at leading Payment Services Provider Ecommpay puts it, “We want Ecommpay to be visible in the rooms where the conversation has a real commercial edge. MPE delivers that, not least of which because the conference programme reflects what’s actually happening in the industry now – as well as focusing on the future.” Emre Talay, founder and CEO of Payrails, agrees: “I learn something new every year. This is the place to come if you want to talk face-to-face with merchants about the problems they face. ”

Emre Talay’s comment above speaks to one of the key attractions of MPE for both merchants and service providers: the ability to foster dialogue on what’s happening now – and what’s coming next. While agentic commerce, possibly the most talked-about subject in payments at present, was obviously prevalent, experts we spoke to shared a number of other concerns that are currently preoccupying merchants.

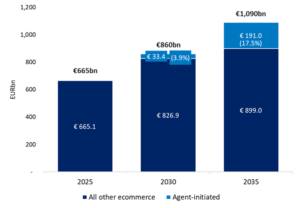

As to Agentic itself, something of the “elephant in the room” this year, Tieto Banktech predicts that Agentic commerce could be used for one in five transactions by 2035[1]. According to Mastercard’s EVP Core Payments for Europe, Brice Van de Waal de Ghelcke, agentic is “the biggest issue facing merchants right now. At present, it’s about defining the specifications and interface, and how best to capture a customer’s intent when they instruct an agent, which is, after all, a new element in the payments ecosystem.”

Others interviewed for this piece agree about agentic’s significance – but go on to note some downside risks associated with agentic, such as the implications of agentic transactions for fraud management and the risk that agents might cause merchants to lose brand value if consumers are unaware of offers and deals executed on their behalf.

“A recent Visa study recorded a 25% global increase (40% in the US) in malicious bot-initiated transactions in 2025.”

The risks associated with agentic are real – and growing. A study by MPE sponsor Visa, published in early 2026, recorded a 25% global increase in malicious bot-initiated transactions in the six months leading into late 2025[2]. Agentic commerce flows are expected to accelerate this fraud trend as criminals exploit agentic commerce by injecting false prompts injection, stealing customer tokens, or using deepfake software to impersonate customers. As a guide to how bad things might get, dark web discussions of “AI agents” are reported to have risen by more than 450% in the last six months of 2025.[3]

Some skepticism regarding the benefits of agentic transactions for merchants was also noted by those we spoke to for this article. Emre Talay, Founder and COO of Payrails, said that “there’s a kind of limbo around agentic payments … is this a bubble? One question is what can it actually do for merchants? Right now, merchants are most focused on how to take advantage of value-added services over and above processing and transaction management.”

Essentially, taking advantage of value-added services comes down to driving better revenue and profitability by improving the number of browsing shoppers who can be converted into purchasers – also known as conversion. To achieve this, merchants need to understand which payment methods perform best for them at checkout, and ensure their checkout process is as smooth and secure as possible. Robert Kraal, Co-Founder, Business Development at cloud-based card payment processing platform Silverflow, says: “maximising conversions is one of the biggest issues facing merchants right now, alongside preparing for agentic commerce; and how to optimise their acceptance strategy for the right payment solutions is a big part of that.”

For James Churchill, General Manager of Global Brands at global payment services platform Rapyd, improving conversions involves “building consumer trust and confidence in the authentication and authorisation of transactions – which also drives higher customer satisfaction.” James also added that he expects new payment methods, such as crypto, to play a bigger role in the near term. Statistics from Chainalysis back up this claim, with a 125% increase reported in transactions using crypto-currencies between 2024 and 2025[4], and more than $4 trillion dollars stored in crypto world-wide – a greater figure than the total GDP of the UK or France.

“Total value stored in crypto is now greater than the GDP of the UK or France.”

If everyone’s interested in agentic, even if they don’t agree what will happen with it, then there’s much less debate around the challenges faced by merchants when it comes to market fragmentation. Merchants are having to deal with an ever-growing range of payment options preferred by consumers, not to mention technology which is changing faster than they are able to keep up. Breno Oliveria, Chief Product Officer at Payabl, describes market fragmentation as “a real challenge facing merchants at present. One question for the payments industry is how we help merchants capture as many payment methods as possible, at the same time helping them to overcome any technology debt and achieve better synergy between their in-person payments and online checkout experiences.”

Despite much debate about the role of agentic commerce, more than half of the experts we spoke to at MPE 2026 felt that AI – in terms of the application of smart algorithms to transaction data, tokenisation and other areas of payments – would be the big story eighteen months from now, rather than agentic commerce per se. Yawar Hussain, Head of Product Solutions at Juspay, comments: “We can expect software development of all kinds to get cheaper thanks to AI. As that happens, merchants will look to re-tool their checkout experiences thanks to the reduced cost of doing so. We may also start to see agentic commerce start to scale by the end of 2027, so some merchants who have not prepared could find themselves playing catch-up.”

“AI could reduce onboarding costs like KYC and ID authentication by 50% in the next few years.” – Boston Consulting Group

Reductions in software development costs are realised not through hiring fewer developers – though that could be a future outcome – but by improving the efficiency of software development, making features, bug fixes and new releases cheaper to realise as AI takes on more of the “grunt work”, drafting simple subroutines and suggesting fixes. Software developer EncodeDots estimates the current reduction in AI development costs to be in the region of 30-40% over the last two to three years[5] – a significant saving which will certainly empower both merchants and payments companies to undertake improvements in their offering.

For Ecommpay’s Miranda McLean, payments companies should expect AI to have a definitive effect on the customer experience, improving consumer trust in those merchants able to use AI to improve the customer experience: “As AI becomes embedded in customer journeys, the question of whether consumers trust the experience they’re having will become a defining competitive differentiator. Merchants who have invested in transparency, accessibility, and genuine customer-centricity will be the winners.”

Across the board, our experts project that 2027 will be the year AI delivers sweeping change in payments, with Payrails’ Emre Talay stating that “by the end of 2027, AI will still dominate the narrative. We’ll see the creation of more AI-driven insights from rich transaction data, further growth in tokenisation and some business routines (such as KYC) being transformed by AI.”

According to a report from the Boston Consulting Group[6], AI will transform Know Your Customer (KYC) routines in payments by automating identity verification at onboarding, introducing automated risk assessment and customer profiling thanks to access to vast, anonymised datasets, and improving routines associated with sanctions and Politically Exposed Persons (PEP) screening. As with software development, BCG project that AI will also deliver cost savings of up to 50% in KYC and customer authentication, though it’s expected that the efficiency gains – in terms of time and money – will be more valuable than the cost savings themselves.

Not all changes over the next eighteen months will necessarily be linked to AI. Mastercard’s Brice Van de Waal de Ghelcke sees a complete overhaul of merchant processes as merchants use the cheaper software development costs mentioned earlier to play catch-up: “We’ll see increased focus on merchant processes and data infrastructure, as these catch up with the last 20 years of developments in e-commerce. Fraud will remain an issue, and improving user experience, too. This means examining every detail of the user experience, including reviews and product information, post-transaction return policies and more.”

One interesting take on the future comes from Silverflow’s Robert Kraal, who expects merchants to become more self-reliant in terms of back-office processes such as Accounts Receivable, in a development which possibly reflects both the rise of AI and growing merchant awareness of the importance of payments to their business as a whole: “A year from now, merchants will be looking to do more themselves – whether that’s reconciling invoices and payments, cash management or in other areas. They will also be looking to insource certain activities, including risk management and optimising pricing to deliver maximum conversions – driving a 90% conversion rate to 92%, for example. They will also be looking to do this while reducing the number of parties involved in the transaction chain.”

Examples of what Robert refers to as merchant insourcing could include in-house banking models such as global pharmaceutical giant Roche’s decision to centralise its cash pooling, liquidity management and inter-company transfers into a single treasury function – a move copied by other giants such as Microsoft and Electrolux. This gives major international companies more control over their cash and makes them less dependent on banks, while dramatically reducing the fees they pay third parties.

As business-to-business (B2B) marketplaces continue to rise, with an article by strategy consultants KoreFusion projecting turnover will reach US$18.6 trillion by the end of 2026[7], we should expect to see such players (think Etsy, eBay, Alibaba and many more) look to handle merchant payouts more on their own, and likewise to handle more of the cash management process, with the same goals as the big international companies mentioned above – to gain more control over cash, reduce their dependency on banks, and cut the level of fees they pay third parties.

Discussion of all of the above themes was made possible by MPE’s unique format, which fosters debate and encourages engagement between participants – whether that’s over coffee, in a 1-1 meeting, or during a breakout.

While those we interviewed praised many aspects of MPE 2026, from the strength of its agenda through to the quality of panel discussions and high-profile keynote speakers, stand-out features of the conference – aside from the opportunity for continuous, informal networking – were firstly, the ability to meet customers face-to-face, and secondly, the high-quality round tables featuring candid, honest insights into the future of payments.

Rapyd’s James Churchill says, “hosted customer meetings and round-tables are the features we value most. In particular, we value the ability to engage with customers in person.” Ecommpay’s Miranda McLean agrees: “The hosted meeting format has obvious commercial value, but it’s the roundtables where I learn the most. A group of thought leaders around a table, Chatham House rules – you simply don’t get the insight and honesty from a stage presentation.”

“hosted customer meetings and round-tables are the features we value most. In particular, we value the ability to engage with customers in person.” – James Churchill, Rapyd

Above all, though, it appears our interviewees value MPE as the outstanding opportunity to meet their contacts and make new ones in a face to face environment. As Romy Mor, Business Development Manager for the UK and France at Riskified puts it, “Personal contact is everything in the age of AI – meaning human connections and conversations. As people work from home and over the internet more, the value of personal contact has only increased. For us, that’s a big advantage of coming to MPE.”

Indeed, in the digital era it would appear that senior executives value human contact more than ever – whether that’s chance meetings in corridors, formal meetings with customers, or engaging and being challenged by other professionals. To give the last word to Mastercard’s Brice Van de Waal de Ghelcke: “the ability to meet people in person surpasses any kind of digital connection. As we work together to build complex payments ecosystems, it’s important to develop personal relationships and connect with people to foster collaborative partnerships.”

Amen to that – and see you at MPE 2027, which runs between 9 and 11 March next year in Berlin!

James Wood is the Founder of Eris Intelligence, a specialist consultancy in market research, content creation, design and distribution services for the payments, banking and financial technology sectors. www.erisintelligence.co.uk

[1] Tieto Banktech, 7 October 2025: “A-commerce agents: all change for payments?”: https://www.tietoevry.com/en/blog/2025/10/a-commerce-agents-all-change-for-payments/

[2] Visa, 20 November 2025: “Agentic Commerce: the threat landscape”: https://corporate.visa.com/en/sites/visa-perspectives/security-trust/the-threats-landscape-of-agentic-commerce.html

[3] Signifyd, 17 February 2026: “Agentic Commerce Fraud: Risks, Tactics and Prevention”: https://www.signifyd.com/blog/agentic-commerce-fraud/

[4] Chainalysis, 2 September 2025: “2025 Geography of Cryptocurrency Report”: https://www.chainalysis.com/blog/2025-global-crypto-adoption-index/

[5] See LinkedIn post, 27 February 2026: “How AI is reducing development costs by 30-40%”: https://www.linkedin.com/pulse/how-ai-reducing-development-costs-3040-encodedots-dyohf/

[6] BCG, 24 October 2025: “The Know-Your-Customer Agentic AI Revolution.” https://www.bcg.com/publications/2025/know-your-customer-agentic-ai-revolution

[7] KoreFusion, 14 March 2025: “B2B Marketplaces: An Emerging Market Phenomenon That’s Going Global”

https://www.korefusion.com/insights/b2b-marketplaces-an-emerging-market-phenomenon-thats-going-global